Disclosures

Disclosures & Policies

Our commitment to preserving and protecting the privacy and security of your personal information is one of our fundamental missions.

We’re confident that our strong security controls ensure that your information is protected. We consistently monitor and improve our verification process to protect against unauthorized access to personal information.

ATM Fees*

ATM Transaction Fees

– at DuTrac-owned ATMs No Charge

– at ATMs not owned by DuTrac and at Point Of Sale terminals $1.50

*DuTrac-owned ATMs and those ATMs associated with the Privileged Status Network do not charge an ATM surcharge fee.

Lost Credit/Debit Card Fee $20.00 per card

Rush Lost Credit/Debit Card Fee $45.00 per card

Lost SecureCard Replacement $7.00 per card

PIN-Based Debit Card Fees**

**First 12 transactions per month at no charge, $1.50+tax after first 12 for Relationship Checking and High Yield Checking accounts.

Eco Plus Account subscribers receive free unlimited, ATM transactions at DuTrac-owned or those ATMs associated with the Privileged Status Network

Securely access, monitor and pay bills on-time, accurately and on the dates when you want bills paid through DuTrac’s Bill Pay. Bill Pay is a digital bill paying solution, at no cost to members, only requiring a subscription to e-Banking, DuTrac’s online banking service or MobileLink, DuTrac’s banking app. An introduction and instructions for setting up Bill Pay reside with these two banking resource portals. Please contact a financial services representative with more information or to have your questions answered.

This agreement governs the use of your Online Bill Pay Service.

By enrolling in Bill Pay, you hereby authorize DuTrac Community Credit Union to make payments on your behalf by debiting the designated checking account and transferring the funds to the designated merchant accounts as indicated. The agreements, rules, and regulations applicable to your checking, savings accounts and other accounts, serviced by your credit union, remain in effect and continue to be applicable, except as specifically stated in this agreement.

Disclosure of Procedures and Fees

By accepting this agreement, you will be billed for the Online Bill Pay service based on the following fee plan.

Online BillPay is a FREE SERVICE. There are no monthly fees or per items fees for using the service. You should also sign up for and use online e-statements, also a free online service from DuTrac Community!

When scheduling payments, please allow three business days for an electronic payment and seven business days if paying by check. (Choose a payment date at least three days prior to the due date on your bill when paying electronically.)

Scheduled payments that fall on a Saturday or Sunday will be paid on Monday.

Open payee enrollment gives members unlimited capacity to add payees. In order to establish a level of quality control, your payees will be notified. Successful notification can take up to four days. Therefore, when setting up a payment for a new payee, please wait until the Payee Status reads “available.”

Fees described above apply to the use of Internet Bill Pay. Additional fees may be incurred for late payments or insufficient funds on your account. These fees are $32.50 per item. There is no limit to the number of payees and/or payments that you can set up using this service.

NSF (non-sufficient funds) Fee $30.00 per item

Overdraft Fee (View this disclosure below) $30.00 + tax per item

Stop Payment Fee $30.00 + tax per request

Automatic Overdraft Transfer $5.00 + tax per transfer or advance

Automatic Loan Advance $5.00 + tax per transfer or advance

Check Fee (Relationship Checking) $.10 each + tax

(After first 40 per month at no charge.)

Check Fee (High Yield Checking) $.10 each + tax

(After first 20 per month at no charge.)

Check Copy $2.00 + tax per check

Check Printing Fee Prices vary depending on style

This is how we will handle information we learn about you from your visit to our website. The information we receive depends upon what you do when visiting our site.

If you visit our site to read or download information:

We collect and store only the following information about you: the name of the domain from which you access the Internet (for example, aol.com, if you are connecting from an America Online account); the date and time you access our site; and the Internet address of the website from which you linked directly to our site.

We use the information we collect to measure the number of visitors to the different sections of our site, and to help us make our site more useful to visitors.

If you identify yourself by sending an email:

You also may decide to send us personally identifying information in an electronic mail message. We will respond to your email as appropriate and may keep your email address for the purpose of sending information pertinent to DuTrac Community Credit Union.

Although we may retain your email address we will not sell, give, or in any way share, your personally identifying information to any third-party vendor or to any other organization.

Effective July 1, 2025

This e-Banking Agreement and Disclosure (“Agreement”) is the contract which covers your and our rights and responsibilities concerning the e-Banking services offered to you by DuTrac (“DuTrac Community Credit Union”). The e-Banking service permits you to electronically initiate account transactions involving your accounts and communicate with DuTrac Community Credit Union. In this Agreement, the words “you”, “your” and “yours” mean those who request and use e-Banking, any joint owners of accounts accessed under this Agreement or any authorized users of this service. The words “we,” “us,” and “our” mean the Financial Institution. The word “account” means any one or more accounts you have with DuTrac Community Credit Union. By requesting and using the e-Banking service, each of you, jointly and severally, agree to the terms and conditions in this Agreement, and any amendments.

e-Banking Service

Account Access If we approve your application for the e-Banking service, you may use your personal computer to access your accounts. You must use your access code along with your account number to access your accounts. The e-Banking service is accessible seven (7) days a week, twenty-four (24) hours a day. You will need a personal computer, direct dial modem and access to the Internet (World Wide Web). You are responsible for the installation, maintenance and operation of any software and your computer. DuTrac Community Credit Union will not be responsible for any errors or failures involving any telephone service, Internet service, software installation or your computer.

Types of Transactions At the present time, you may use the e-Banking service to:

- Transfer funds between your checking, savings and loan accounts.

- Transfer funds to accounts of other members you authorize for any of your accounts.

- Review account balance, transaction history and tax information for any of your checking, savings or loan accounts.

- Request a withdrawal from any checking, savings, or loan account by check mailed to you.

- Conduct other transactions permitted by DuTrac Community Credit Union.

- Communicate with DuTrac Community Credit Union using the electronic mail (“Email”) feature.

Transactions involving your deposit accounts, including checking account stop payment requests, will be subject to the terms of your account agreement and transactions involving a line of credit account will be subject to your loan agreement and disclosures, as applicable.

Service Limitations

The following limitations on e-Banking transactions may apply in using the services listed below:

- Transfers You may make funds transfers to other accounts of yours as often as you like. You may transfer or withdraw up to the available balance in your account or up to the available credit limit on a line of credit at the time of the transfer, except as limited under this Agreement or your deposit or loan agreements. DuTrac Community Credit Union reserves the right to refuse any transaction that would draw upon insufficient or unavailable funds, lower an account below a required balance, or otherwise require us to increase our required reserve on the account.

- Account Information The account balance and transaction history information may be limited to recent account information involving your accounts. Also, the availability of funds for transfer or withdrawal may be limited due to the processing time for ATM transactions and our Funds Availability Policy.

- Email DuTrac Community Credit Union may not immediately receive email communications that you send and DuTrac Community Credit Union will not take action based on email requests until the Financial Institution actually receives your message and has a reasonable opportunity to act. If you need to contact DuTrac Community Credit Union immediately regarding an unauthorized transaction or stop payment request, you may call DuTrac Community Credit Union at the telephone number set forth in the Liability for Unauthorized Access section.

Security of Access Code

The personal identification number (PIN) or access code (“access code”) issued to you is for your security purposes. The access code is confidential and should not be disclosed to third parties or recorded. You are responsible for safe keeping your access code. You agree not to disclose or otherwise make your access code available to anyone not authorized to sign on your accounts. If you authorize anyone to use your access code that authority shall continue until you specifically revoke such authority by notifying DuTrac Community Credit Union. If you fail to maintain the security of these access codes and DuTrac Community Credit Union suffers a loss, we may terminate your e-Banking and account services immediately.

Liability For Unauthorized Access

You are responsible for all transfers and bill payments you authorize under this Agreement

- If you permit other persons to use the e-Banking service or your access code, you are responsible for any transactions they authorize or conduct on any of your accounts. However, tell us at once if you believe anyone has used your access code or accessed your accounts through e-Banking without your authorization. Telephoning is the best way of keeping your possible losses down.

- If you tell us within two (2) business days, you can lose not more than fifty dollars ($50) if someone accesses your accounts without your permission.

- If you do not tell us within two (2) business days after you learn of the unauthorized use of your account or access code, and we can prove that we could have stopped someone from accessing your account without your permission if you had told us, you could lose as much as five hundred dollars ($500.00).

- If your statement shows e-Banking transfers that you did not make, tell us at once. If you do not tell us within sixty (60) days after the statement was mailed to you, you may not get back any money lost after the sixty days (60) if we can prove that we could have stopped someone from making the transfers if you had told us in time.

- If a good reason (such as a hospital stay) kept you from telling us, we will extend the time periods.

If you believe that someone has used your access code or has transferred or may transfer money from your account without your permission, call DuTrac Community Credit Union at: (563) 582-1331 or write:

DuTrac Community Credit Union P.O. Box 3250 Dubuque, Iowa 52004-3250.

In IOWA, you may be required to provide written notice to us concerning any unauthorized transfer.

Business Days

Our business days are Monday through Friday. Holidays are not included.

Fees and Charges

There are certain charges for e-Banking services as set forth on DuTrac Community Credit Union’s Fee Schedule. From time to time, the charges may be changed. We will notify you of any changes as required by law. If you request a transfer or check withdrawal from your line of credit account, such transactions may be subject to charges under the terms and conditions of your loan agreement.

Periodic Statements

Transfers, withdrawals, and bill payments transacted through e-Banking will be recorded on your periodic statement. You will receive a statement monthly unless there is no transaction in a particular month. In any case, you will receive a statement at least quarterly.

Account Information Disclosure

We will disclose information to third parties about your account or the transfers you make:

- As necessary to complete transfers and bill payments;

- To verify the existence of sufficient funds to cover specific transactions upon the request of a payee or a third party, such as a credit bureau or merchant;

- To comply with government agency or court orders;

- If you give us your written permission.

DuTrac Community Credit Union’s LIABILITY FOR FAILURE TO MAKE TRANSFERS.

If we do not complete a transfer to or from your account on time or in the correct amount according to our agreement with you and the instructions you transmit, we will be liable for your actual losses or damages. However, the Financial Institution will not be liable:

- If, through no fault of ours, you do not have adequate funds in your account to complete a transaction, your account is closed, or the transaction amount would exceed your credit limit on your line of credit, if applicable.

- If you used the wrong access code or you have not properly followed any applicable computer, Internet Access, or DuTrac Community Credit Union user instructions for making transfer and bill payment transactions.

- If your computer fails or malfunctions or the e-Banking service was not properly working and such problem should have been apparent when you attempted such transaction.

- If circumstances beyond our control (such as fire, flood, telecommunication outages, postal strikes, equipment or power failure) prevent making the transaction.

- If the funds in your account are subject to an administrative hold, legal process or other claim.

- If you have not given DuTrac Community Credit Union’s complete, correct and current instructions so the Financial Institution can process a transfer or bill payment.

- If the error was caused by a system beyond DuTrac Community Credit Union’s control, such as your Internet Service Provider.

- If you do not authorize a bill payment soon enough for your payment to be made and properly credited by the payee by the time it is due.

- If DuTrac Community Credit Union makes a timely bill payment but the payee nevertheless does not credit your payment promptly after receipt.

- If there are other exceptions as established by DuTrac Community Credit Union from time to time.

Termination of e-Banking Services

You agree that we may terminate this Agreement and your use of the e-Banking services if you or any authorized user of your account or access code breach this or any other agreement with us; or if we have reason to believe that there has been an unauthorized use of your account or access code.

You or any other party to your account can terminate this Agreement by notifying us in writing. Termination of service will be effective the first business day following receipt of your written notice. However, termination of this Agreement will not affect the rights and responsibilities of the parties under this Agreement for transactions initiated before termination.

Notices

The DuTrac Community Credit Union reserves the right to change the terms and conditions upon which this service is offered. The DuTrac Community Credit Union will mail notice to you at least twenty one (21) days before the effective date of any change, as required by law. Use of the e-Banking service is subject to existing regulations governing your accounts and any future changes to those regulations.

Billing Errors

In case of errors or questions about your e-Banking transactions, telephone us at the phone number or write to us at the address set forth above in the Liability for Unauthorized Access section as soon as you can. We must hear from you no later than sixty (60) days after we sent the first statement on which the problem appears.

Tell us your name and account number. Describe the transaction you are unsure about and explain as clearly as you can why you believe it is an error or why you need more information.

Tell us the dollar amount of the suspected error.

- If you tell us orally, we may require that you send us your complaint or question in writing within ten (10) calendar days. We will determine whether an error occurred within ten (10) business days after we hear from you and we will correct any error promptly.

- If we need more time, however, we may take up to forty-five (45) days to investigate your complaint or question.

- If we decide to do this, we will credit your account within ten (10) business days for the amount you think is in error, so that you will have the use of the funds during the time it takes us to complete our investigation.

- If we ask you to put your complaint or question in writing and we do not receive it within ten (10) business days, we may not credit your account.

We will tell you the results within three (3) business days after completing our investigation. If we decide that there was no error, we will send you a written explanation. You may ask for copies of the documents that we used in our investigation.

- If a notice of error involves an electronic fund transfer that occurred within thirty (30) days after the first deposit to the account was made, the applicable time periods for action shall be twenty (20) business days in place of ten (10) business days.

- If a notice of error involves an electronic fund transfer that was initiated in a foreign country or occurred within thirty (30) days after the first deposit to the account was made, the applicable time period for action shall be ninety (90) calendar days in place of forty five (45) calendar days.

Enforcement

You agree to be liable to DuTrac Community Credit Union for any liability, loss, or expense as provided in this Agreement that DuTrac Community Credit Union incurs as a result of any dispute involving your accounts or services. You authorize DuTrac Community Credit Union to deduct any such liability, loss, or expense from your account without prior notice to you. In the event either party brings a legal action to enforce the Agreement or collect any overdrawn funds on accounts accessed under this Agreement, the prevailing party shall be entitled, subject to applicable law, to payment by the other party of its reasonable attorney’s fees and costs, including fees on any appeal, bankruptcy proceedings, and any post-judgment collection actions, if applicable.

Governing Law

This Agreement shall be governed by and construed in accordance with all applicable federal laws and all applicable substantive laws of the state where you opened your account, and the Bylaws of the Credit Union as they now exist or may be hereafter amended. You understand that we must comply with these laws, regulations, and rules. You agree that if there is any inconsistency between the terms of the Agreement and any applicable law, regulation, or rule, the terms of this Agreement will prevail to the extent any such law, regulation, or rule may be modified by agreement between us.

An In-House Loan is a loan that remains with, and is serviced by, DuTrac Community Credit Union for the entire term of the loan. During the life of your loan, if you have questions, we are right here to assist you.

- Local processing and underwriting, with mortgage consultants available to answer your questions.

- Fixed rate loans are available with a variety of loan terms, including 10, 15, 20 and 30 years.

- No pre-payment penalties

Fixed Rate Conventional Loan

A fixed rate conventional loan is a mortgage with a set interest rate that remains the same for the duration of the loan. A portion of the payment goes toward the principal, and the rest is interest.

Construction Loans

Take out a construction loan for your new home build. We offer a two-time construction loan process, the first loan is the construction loan that offers a 9 month balloon with interest only payments. After construction is complete you can refinance the construction loan into permanent fixed rate financing.

Lot Loans

Lot loans can help finance the purchase of land with the intention of building a home on the property, the land must be in an eligible area. The lot loan terms are a three year balloon with principal and interest payments due.

Loan Modification

A loan modification is offered to members that have a current mortgage loan with DuTrac. The loan modification is similar to a rate term refinance, we will modify the rate to a lower rate that the member must qualify for based on the current market rate at the time of application. The term will stay on the same amortization or you can choose to lower the term. The costs are reduced from a full refinance option.

Rental/Investment Property Loans

We have loans available for the purchase or refinance of a 1-4 family, rental property. These loans require a 20% down payment and are typically amortized over 25 years, with a balloon maturity date of either 3, 4, 5, 7 or 10 years. At your balloon maturity date, you must either apply with DuTrac to renew your loan or pay off your loan by refinancing it with another lender or by other means.

Mortgage Refinance

A mortgage refinance is when you replace your current mortgage with a new one. We will refinance mortgages currently held by other servicers or current DuTrac mortgages. We offer both a rate term refinance option and a cash out refinance option. The cash out mortgage is an option to tap into your homes equity.

Minimum floor rate applies. Offer only on secured consumer loans from another financial institution transferred to DuTrac. Loan payments must be current and standard credit criteria apply. Does not apply to real estate, home equity, business loans, credit cards, share secured loans or lines of credit.

To qualify for membership at DuTrac Community Credit Union you must meet certain eligibility requirements. Member Advantage offer applies to secured consumer loans brought into DuTrac Community Credit Union from another financial institution. Loan approval is subject to DuTrac’s normal underwriting guidelines and some restrictions apply. Loan payments must be current and standard credit criteria apply. Does apply to real estate, home equity, business loans, credit cards, share secured loans or lines of credit. Your savings may vary depending on remaining balance, term of the loan and APR (Annual Percentage Rate) you are currently paying. Contact a financial services consultant for the current minimum rate available for this program.

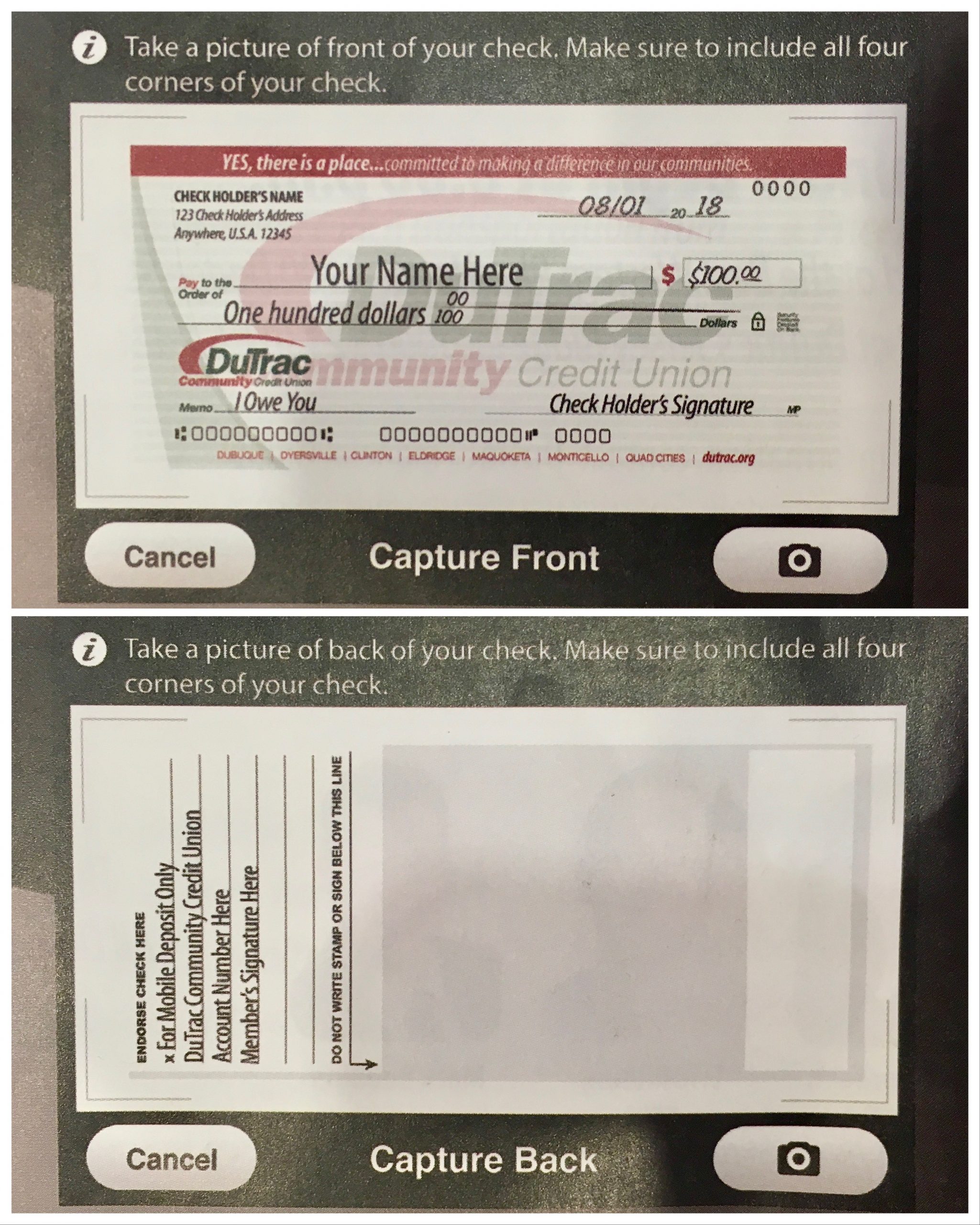

Mobile Deposit

This Mobile Deposit (“Agreement”) contains the terms and conditions for the use of Mobile Deposit that DuTrac Community Credit Union (“Credit Union”, “us,” or “we”) may provide to you (“you,” or “User”). Other agreements you have entered into with Credit Union, including your Membership, as amended from time to time, are incorporated by reference and made a part of this Agreement.

- Services: The Mobile Deposit (“Services”) allows you to make deposits to your checking, savings, or money market savings accounts from home or other remote locations by scanning checks and delivering the images and associated deposit information to Credit Union or Credit Union’s designated processor.

- Acceptance of these Terms: Your use of the Services constitutes your acceptance of this Agreement. This Agreement is subject to change from time to time. We will notify you of any material change via email, text message, or on our website(s) by providing a link to the revised Agreement or by an online secure message. You will be prompted to accept or reject any material change to this Agreement the next time you use the Service after Credit Union has made the change. Your acceptance of the revised terms and conditions along with the continued use of the Services will indicate your consent to be bound by the revised Agreement. Further, Credit Union reserves the right, in its sole discretion, to change, modify, add, or remove portions from the Services. Your continued use of the Services will indicate your acceptance of any such changes to the Services.

- Limitations of Service: When using the Services, you may experience technical or other difficulties. We will attempt to post alerts on our website or send you a text message to notify you of these interruptions in Service. We cannot assume responsibility for any technical or other difficulties or any resulting damages that you may incur. Some of the Services have qualification requirements, and we reserve the right to change the qualifications at any time without prior notice. We reserve the right to change, suspend or discontinue the Services, in whole or in part, or your use of the Services, in whole or in part, immediately and at any time without prior notice to you.

- Hardware and Software: In order to use the Services, you must obtain and maintain, at your expense, compatible hardware and software as specified by Credit Union from time to time. Credit Union is not responsible for any third party software you may need to use the Services. Any such software is accepted by you as is and is subject to the terms and conditions of the software agreement you enter into directly with the third party software provider at time of download and installation.

- Eligible Items: You agree to scan and deposit only “checks” as that term is defined in Federal Reserve Regulation CC (“Reg. CC”). When the image of the check transmitted to Credit Union is converted to an Image Replacement Document for subsequent presentment and collection, it shall thereafter be deemed an “item” within the meaning of Articles 3 and 4 of the Uniform Commercial Code.

You agree that you will not scan and deposit any of the following types of checks or other items which shall be considered ineligible items:

- Checks payable to any person or entity other than the person or entity that owns the account that the check will be deposited.

- Checks containing an alteration on the front of the check or item, or which you know or suspect, or should know or suspect, are fraudulent or otherwise not authorized by the owner of the account on which the check is drawn.

- Checks payable jointly, unless deposited into an account in the name of all payees.

- Checks previously converted to a substitute check, as defined in Reg. CC.

- Checks drawn on a financial institution located outside the United States.

- Checks that are remotely created checks, as defined in Reg. CC.

- Checks not payable in United States currency.

- Checks dated more than six months prior to the date of deposit.

- Checks or items prohibited by Credit Union’s current procedures relating to the Services or which are otherwise not acceptable under the terms of your Credit Union account.

- Checks payable on sight or payable through Drafts, as defined in Reg. CC.

- Checks with any endorsement on the back other than that specified in this agreement.

- Checks previously been submitted through the Service or through a remote deposit capture service offered at any other financial institution.

- Checks or items that are drawn or otherwise issued by the U.S. Treasury Department

- Checks that are prohibited by the Credit Union’s current Membership Agreement with you

- Checks that are in violation of any federal or state law, rule, or regulation.

- Endorsements and Procedures. You agree to legibly endorse all items transmitted through this service with:

For Mobile Deposit Only

Credit Union Name

Account Number

Member’s Signature

Additionally, you agree to follow any and all other procedures and instructions for use of the Services as Credit Union may establish from time to time.

| Returned Mail Fee | $5.00 |

| Account Research Fee | $15.00 per hour + tax ($15 minimum) |

| Account Balancing Fee | $20.00 per hour + tax (1st 15 min. free) |

| Membership Reopen Fee (Applies to memberships closed in previous 12 months) | $15.00 |

| Return Item Fee | $30.00 per occurrence |

| Check Collection Fee | $25.00 per check |

| Canadian Check Collection Fee | $25.00 per check |

| Unreadable MICR Line Fee | $1.00 per check |

| Domestic Wire Transfers (outgoing) | $25.00 per transfer (in person) $30.00 per transfer (phone requests) |

| Foreign Wire Transfers (outgoing) | $50.00 per transfer (in person) $55.00 (phone requests) |

| Incoming Wire Transfer Fee | $10.00 per incoming wire |

| Money Order Fee | $3.00 each |

| Official Check Fee | $3.00 each |

| Statement History | $1.00 per page |

| Fax Fee | $1.00 per page |

| Copy Fee | $.10 per page |

| Inactive Relationship Fee (Total relationship less than $100 and no activity in previous 12 months. Does not apply to members under age 18) | $15.00 per quarter |

| Check Cashing Fee | $5.00 or 1% of amount of check if less than $100 in membership account |

| Notary Fee | $5.00 per document to be notarized for a non-member and $5.00 per loan document from another financial institution. |

| Signature Guarantee | Free to members |

| Compliance with Garnishments, Levies | $50.00 |

| IRA Direct Transfer Fee | $25.00 per IRA transfer |

| 12/21/2015 | |

| Safe Deposit Box Fees | |

| Annual Box Rental Sizes and rates vary by size and location | |

| Lost Key Fee | $20.00 |

| Box Drilling Fee | Cost of drilling + $20.00 |

| Late Safe Deposit Box Rental Fee | $10.00 |

We understand that unexpected overdrafts occur from time to time—Overdraft Coverage can help. There are three ways to cover overdrafts:

1. Overdraft Protection link to another DuTrac deposit account. Fee: $5 plus tax per transfer. Overdraft Protection applies to all transactions and may help prevent overdrafts by automatically transferring funds to your checking account from another DuTrac account

2. Overdraft Protection line of credit. Fee: $5 plus tax per transfer plus interest. Overdraft Protection applies to all transactions and may help prevent overdrafts by automatically transferring funds to your checking account from a DuTrac line of credit. Please note that an Overdraft Protection line of credit is subject to credit approval.

3. Courtesy Pay Fee: $30 fee plus tax per item. Courtesy Pay allows you to overdraw your account up to the disclosed limit to pay a transaction. Even if you have overdraft protection, Courtesy Pay is still available as a secondary coverage if the other protection source is exhausted. Courtesy Pay is not a line of credit; it is a discretionary overdraft service that can be withdrawn at any time without prior notice.

What is the difference between Standard Coverage vs Extended Coverage?

To receive standard Overdraft Protection and Courtesy Pay, no action is required on your part.

To receive Extended Coverage, which also covers ATM withdrawals and everyday debit card transactions, your consent is required.

Business accounts automatically have Extended Coverage. To receive Extended Coverage, contact us. You can discontinue Courtesy Pay any time by contacting us.

Transactions covered with Standard Coverage Courtesy Pay:

- Checks*

- ACH – Automatic Debits

- Recurring Debit Card Payments

- Online Bill Pay Items

- Internet Banking Transfers

- Telephone Banking

- Teller Window Transactions

Transactions covered with Extended Coverage (Your consent required on consumer accounts.) *

- Checks*

- ACH – Automatic Debits

- Recurring Debit Card Payments

- Online Bill Pay Items

- Internet Banking Transfers

- Telephone Banking

- Teller Window Transactions

- ATM Withdrawals

- Everyday Debit Card Transactions

*If you choose Extended Coverage on your consumer account, ATM withdrawals and everyday debit card transactions will be included with the transactions listed under Standard Coverage. If you already have Extended Courtesy Pay coverage, it is not necessary to request it again. Business accounts automatically have Extended Coverage.

You can discontinue the Courtesy Pay in its entirety by contacting us at (563) 582.1331 or by sending an e-mail to: members@DuTrac.org

To select Extended Coverage for future transactions, contact us:

Call: (563) 582-1331

Email: members@DuTrac.org

Online: Complete the online consent form

Visit: Stop by any office location

Mail: Complete a printed consent form and mail to us at: P.O. Box 3250, Dubuque, IA 52004-3250

You can discontinue the Courtesy Pay in its entirety by contacting us by phone at (563) 582-1331 or e-mail at members@DuTrac.org.

What Else You Should Know

- A link to another account or line of credit may be less expensive option than an overdraft. A single larger overdraft will result in just one fee, as opposed to multiple smaller overdrafts. Use our mobile, internet, and telephone banking services to track your balance. For financial education resources, please visit mymoney.gov.

- The $30 Overdraft Fee plus tax is charged for each item paid, and a $30 Return Draft Fee is charged for each returned item. If multiple items overdraw your account on the same day, each item will be assessed an appropriate Overdraft Fee or a Return Draft Fee of $30. All fees and charges will be included as part of the Courtesy Pay limit amount. Your account may become overdrawn more than the Courtesy Pay limit amount because of a fee.

- Recipients of federal or state benefits payments who do not wish us to deduct the amount overdrawn and the Overdraft Fee from funds that you deposit or that are deposited into your account may call us at (563) 582-1331 to discontinue Courtesy Pay.

- If an item is returned because the Available Balance (as defined below) in your account is not sufficient to cover the item and the item is presented for payment again, DuTrac Community Credit Union (“We”) will charge a Return Draft Fee each time it returns the item because it exceeds the Available Balance in your account. Because we may charge a Return Draft Fee each time an item is presented, we may charge you more than one fee for any given item as a result of a returned item and representment of the item. When we charge a Return Draft Fee , the charge reduces the Available Balance in your account and may put your account into (or further into) overdraft. If, on representment of the item, the Available Balance in your account is sufficient to cover the item we may pay the item, and, if payment causes an overdraft, charge an Overdraft Fee.

- There is no limit on the total Overdraft Fees per day we will charge.

- This describes the posting order for purposes of determining overdrafts. Our general policy is to post items throughout the day and to post ACH credits before debits in the order received. ATM and PIN-based debit card transactions are posted as they are received. Holds for signature-based transactions are placed as the transaction occurs, and signature-based transactions post throughout the day in the order they are received. Paper checks are posted from lowest to highest dollar amount. However, because of the many ways we allow you to access your account, the posting order of individual items may differ from these general policies. Holds on funds (described herein) and the order in which transactions are posted may impact the total amount of Overdraft Fees or Return Draft Fees assessed.

- Courtesy Pay is not a line of credit; it is a discretionary overdraft service that can be withdrawn at any time without prior notice.

- Depositor and each Authorized Signatory will continue to be liable, jointly and severally, for all overdraft and fee amounts, as described in the Membership Guide. The total (negative) balance, including all fees and charges, is due and payable upon demand.

- We may be obligated to pay some debit card transactions that are not authorized through the payment system but which we are required to pay due to the payment system rules, and as a result you may incur fees if such transactions overdraw your account. However, we will not authorize debit card or ATM transactions unless your account’s Available Balance (including Overdraft Coverage Options) is sufficient to cover the transactions and any fee(s).

Understanding your Available Balance

Your account has two kinds of balances: the Actual Balance and the Available Balance.

- We authorize and pay transactions using the Available Balance.

- Your Actual Balance reflects the full amount of all deposits to your account as well as payment transactions that have been posted to your account. It does not reflect checks you have written and are still outstanding or transactions that have been authorized but are still pending.

- Your Available Balance is the amount available to you to use for purchases, withdrawals, or to cover transactions. The Available Balance is your Actual, less any holds due to pending debit card transactions and holds on deposited funds.

- The balance used for authorizing checks, ACH items, and recurring debit card transactions is your Available Balance plus the amount of the Courtesy Pay limit and any available Overdraft Protection.

- The balance used for authorizing ATM and everyday debit card transactions on accounts with Standard Coverage is your Available Balance plus any available Overdraft Protection but does NOT include the Courtesy Pay

- The balance used for authorizing ATM and everyday debit card transactions on accounts with Extended Coverage is your Available Balance plus any available Overdraft Protection and includes the Courtesy Pay

- Because your Available Balance reflects pending transactions and debit holds, your balance may appear to cover a transaction but later upon settlement it may not be sufficient to cover such transaction. In such cases, the transaction may further overdraw your account and be subject to additional overdraft fees. You should assume that any item which would overdraw your account based on your Available Balance may create an overdraft. Note that we may place a hold on deposited funds in accordance with our Membership Guide, which will reduce the amount in your Available Balance.

- Please be aware that the Courtesy Pay amount is not included in your Available Balance provided through online banking, mobile banking or DuTrac Community Credit Union’s regular account statements.

- We will place a hold on your account for any authorized debit card transaction until the transaction settles (usually within two business days) or as permitted by payment system rules. In some cases, the hold may exceed the amount of the transaction. When the hold ends, the funds will be added to the Available Balance in your account. If your account is overdrawn after the held funds are added to the Available Balance and the transaction is posted to the Available Balance, an Overdraft Fee may be assessed.

- Except as described herein, we will not pay items if the Available Balance in your account (including the Courtesy Pay limit, if applicable) is not sufficient to cover the item(s) and the amount of any fee(s).

Understanding Overdraft Privilege Limits

- Courtesy Pay limits of up to $500 or $750 with Direct Deposit are available for eligible consumer checking accounts opened at least 35 days in good standing and up to $1000 for eligible business checking accounts opened at least 60 days in good standing.

- Courtesy Pay may be reduced if you default on any loan or other obligation to us, your account becomes subject to any legal or administrative order or levy, or if you fail to maintain your account in good standing by not bringing your account to a positive balance within thirty-two (32) days for a minimum of one business day. You must bring your account balance positive for at least one business day to have the full Courtesy Pay limit

If you have any questions about Overdraft Protection or Courtesy Pay, please call us at (563) 582-1331 or visit a branch.

DuTrac Community Credit Union is committed to protecting the privacy of its members. Members can help by following simple guidelines:

- Protect your account numbers, card numbers, PINs (personal identification numbers) and passwords.

- Never keep your PIN with your Debit Card, ATM card or credit card that can provide free access to your accounts if your card is lost or stolen.

- Use caution when disclosing your account numbers, social security numbers, etc. to other persons. If someone calls you, explains the call is on behalf of the credit union and asks for your account number, you should be cautious. Official credit union staff will have access to your information and will not need to ask for it.

- Keep your information with us current. It is important that we have current information on how to reach you. If we detect potentially fraudulent or unauthorized activity or use of an account, we will attempt to contact you immediately. If your address or phone number changes, please let us know.

The rates and terms applicable to your account at DuTrac Community Credit Union are provided in this Rate and Fee Schedule. The Credit Union may offer other rates and fees for these accounts from time to time. Additional Truth in Savings information will be found in your membership manual. Nature of Dividends – Dividends are paid from current income and earnings after required transfers to reserves at the end of the dividend period.